Michael Hyatt became a self-made millionaire when he was just 25, by building two highly successful tech firms valued in the hundreds of millions. Today, he ranks as one of Canada’s top entrepreneurs, is a celebrated “Dragon” on CBC’s new online sensation Next Gen Den, and is a weekly Business Commentator on CBC News Network. He is also an active investor, speaker and philanthropist. Speaking on leadership, entrepreneurship, the future of tech, and managing change, Michael underscores all his talks with the message that to achieve success you need to prepare for a marathon, not a sprint. Now in his second season on Next Gen Den, the show premiered last night, and Filler magazine caught up with him to get his expert advice on venturing into the competitive world of business:

The monikers for our generation go easy on endearment. It’s evident from the Boomerang label we’ve earned for our habit of returning to whence we came (i.e. mom and dad’s) after a short-lived stint in the “real world” to our Me Me Me Generation tag that tips its hat to a certain propensity for narcissistic behavior—suggested by a trend in fish-faced selfies declaratively hashtagged #blessed—the haters be hating we millennials. While it’s true we ushered in an era dominated by social media (in all its self-obsessed plastic glory) and “celebrity” bloggers—culminating in the unfortunate invention of the selfie stick—it is also our generation that has kick-started (no pun intended) a paradigm shift in everyday communication processes that span the globe and marketplace via ideas, technology and companies built by creative visionaries under 30.

“There is this incredible wave of entrepreneurship going on in just about every major city…I’d like to say in the world,” observes Michael Hyatt, co-founder and Executive Chair of BlueCat, a leading Canadian technology company. A weekly business commentator on the CBC News Network, Hyatt is conversant in the rapidly evolving business landscape, and in the keen eyes of this entrepreneur—who made his millions by age 25—change is good. “We’re going through this revolution now, where it’s not 90% cheaper to start a business today than it was 10-15 years ago, it’s 99%. We’re seeing this generation of millennials that are super bright and talented and their starting innovative companies and there going into traditional business that we thought would just be that way forever, and they’re coming in and tearing them apart and putting them into the cloud and making things hyper efficient. There’s a lot of very exciting things happening in business.”

Hyatt is a champion of the next generation of CEOs, and counts investments in start-ups and his role as a mentor at the Creative Destruction Lab at University of Toronto’s Rotman’s School of Business amongst his contributions to future growth. He also happens to be (would-be-entrepreneurs take note) one of three judges on Next Gen Den, the web spinoff of CBC’s popular Dragon’s Den, where entrepreneurs pitch their business ideas to potential investors, otherwise known as “Dragons.”

The sole carry over from the show’s first season, this season Hyatt shares his Next Gen Den Dragon duties with newbies Harley Finkelstein, chief platform officer (CPO) at Shopify Inc., and Nicole Verkindt, founder of OMX (Offset Market Exchange). Scheduled to premiere in tangent with Dragon Dens on October 7th, the 20 webisode series—available exclusively online at cbc.ca—finds its own audience with a younger demographic of entrepreneurs, proposing ideas with millennial prowess.

In honour of Next Gen Den’s upcoming premiere, we caught up with Hyatt to get his expert advice on venturing into the competitive world of business, while also rounding up a few of our favourite local entrepreneurs (each with an individual and very un-big-box cool factor to their business) to talk inspiration and how they did it. Whatever your stock-in-trade may be, or whether you believe in “decacorns” of the Airbnb, Uber or Snapchat variety or not, the knowledge gleaned from this collective we’ve put together has boom worthy stuff to it. Time to do what we millennials do best: start sharing.

What separates this new generation of entrepreneurs? Is it the rise of a creative class?

The cloud is breaking everything—just imagine every business going to the cloud or utilizing the cloud; that creates a hyper efficiency, and margins and delivery of things. There was a time when people didn’t want the horse and buggy to be taking over things, but it did, and we’re going through another generational shift. If you take a three-year-old and give them a newspaper, they’ll take their hand and move the page like an iPad. We’re seeing this shift to the creative class and we’re seeing so many great start-ups in Toronto and Vancouver and Ottawa and they’re doing really well, and they’re hiring a lot of people. The good news is, not only are these start-ups hiring a lot of people, but once they get going and are successful, they’re paying a lot of money and that’s great for our economy. People are paying taxes and going to restaurants and hotels, and that’s what we need.

When you listen to the pitches, are you more interested in the idea or the passion the entrepreneur has in his/her idea?

I would have to say, I’m interested in both. What happens is that if you bet on the person—if I see a really bright girl or guy come in and they have something great—I know that in 24 months, they’re going to pivot their company in either a small way or a big way a couple of times to get to the right place. What I’m really buying is my thought on a person’s ability to pivot their business. We’d like to say that you would have invested in Google or Airbnb on day one, but you probably wouldn’t have because you didn’t quite see it, and people pivot and make changes. You’re betting 75% on the entrepreneur, 25% on the market and the idea, and could this thing ever make any money. I think there is also a self-interest part in it, like, “am I even interested in this business?” Sometimes I see business that I think they can make money, but I’m just not interested in the space; I don’t think I have anything to add. Being an entrepreneur myself, I always wanted to work with people that wanted to add to my business. When you build a company, you could be in it seven to ten years…you could be in it for a long time. So, when you take on an investor, you’re kind of marrying them for a while, and I have to feel like I can add something.

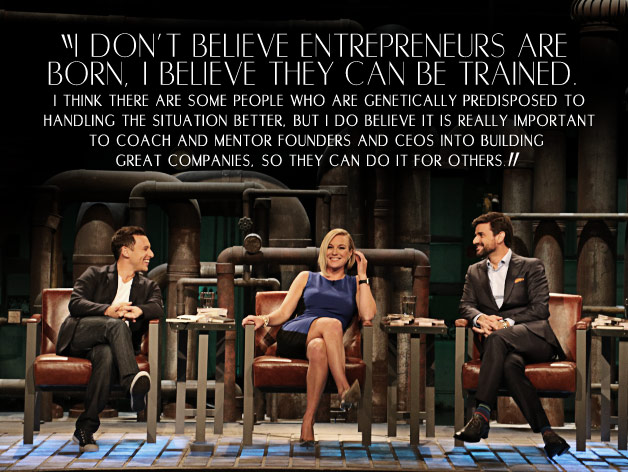

You once said in an interview that a “founder should always run their own business.” What advice can you give to founders dealing with opinionated investors?

Well, investors are opinionated by nature and that’s how they got there. I think it is important for founders to work with people they like. I don’t believe entrepreneurs are born, I believe they can be trained. I think there are some people who are genetically predisposed to handling the situation better, but I do believe it is really important to coach and mentor founders and CEOs into building great companies, so they can do it for others. If I was a young founder in a company, I would try to find people smarter than me that I could work with and think, if I was stuck with them at an airport for four hours, would I be upset, or, would I invite them to my family barbeque? You have to like the person because it is a marriage of sorts, you’re going to be with them for a long time. There’s the high point when you get the money and everyone is high-fiving, but there is going to be a lot of dark days: your product is going to be late, you’re going to miss a quarter of revenue—you may even miss a year of revenue—you’re going to have all these other problems and you’ve got to be able to phone an investor and go, “hey, we just missed our quarter” or “we have a legal problem,” and that someone has to be like, “yeah, I’ve been to that rodeo.” I think that is important.

Do you consider social media to be a critical component of a company’s or product’s success today, or can a company and product still just depend on its good quality to build success?

Social media has allowed for something completely new, which is the network effect. Before when I had a product, it was hard to get it to catch on like fire with word on mouth—like literally word of mouth—now from LinkedIn to Facebook to Twitter to Snapchat and Instagram we have an incredible platform to let a tremendous amount of people know about it very quickly. So, I still think you have to build a great red wagon, as they say, but it will get picked up a lot faster—social media is critical.

What advice would you give an entrepreneur who thinks they have a great idea for a business? What’s one way to gage that something isn’t just a good idea, but a smart business venture?

Well, there’s an unfortunate side to thinking you have a good idea and you have friends and family who love you that will tell you, “oh my God that’s great, do it.” Maybe those are not the people to talk to because they have rose-coloured glasses on; they love you and want you to do well and try, but that’s not the right thing. You need to find people that would naturally invest in your company. Turn around and ask your friends and family for five or ten thousand dollars and you might hear the truth a little bit better. You have to get away from your bias to push and find out will this thing really sell. I would go out and spend a lot of time on people who don’t owe you anything to see if they would buy it.